[ad_1]

WASHINGTON (Reuters) – Democratic and Republican lawmakers on Tuesday pressed Wells Fargo & Co Chief Executive Tim Sloan for proof the bank has put a string of consumer abuse scandals behind it at a tense congressional hearing that saw Sloan firmly on the defensive.

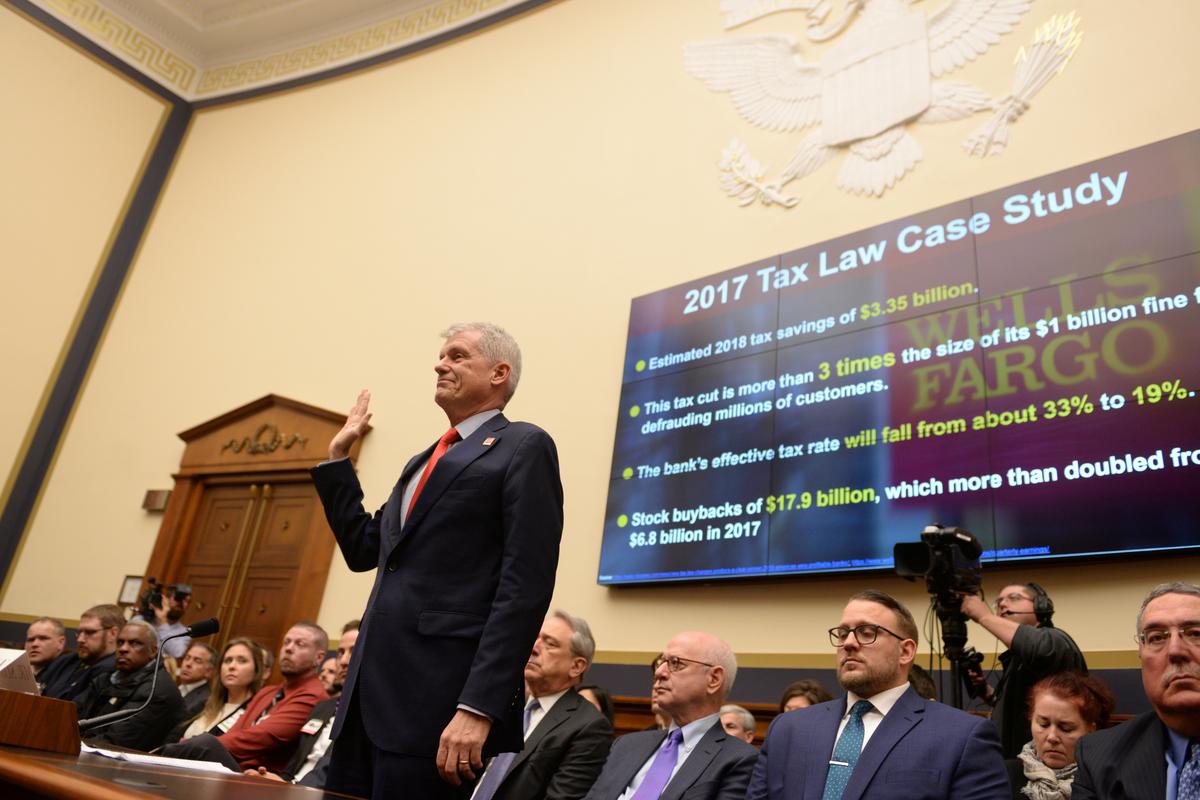

Wells Fargo’s CEO Tim Sloan is sworn in before testifying in a House Financial Services Committee hearing titled: “Holding Megabanks Accountable: An Examination of Wells Fargo’s Pattern of Consumer Abuses” in Washington, U.S. March 12, 2019. REUTERS/Erin Scott

While Sloan struggled to convince skeptical lawmakers that Wells Fargo has transformed its culture, he managed to navigate a hostile committee without a major stumble that would have compounded doubts about his leadership.

One of the harshest blows was dealt after the hearing by a key regulator, which said in a statement it was “disappointed” Wells Fargo had not made more progress fixing its corporate governance and risk management.

Sloan was the first bank executive to be grilled by the House Financial Services Committee since it was taken over by Democrats following the 2018 congressional election. A nervous Wall Street has been keen to see how the panel will treat the industry.

The CEOs of Morgan Stanley, Goldman Sachs Group Inc, Citigroup Inc, JPMorgan Chase & Co and Bank of America Corp are expected to appear before the panel next month.

The committee, led by bank critic Maxine Waters, has several freshmen Democrats who took swipes at Sloan including Alexandria Ocasio-Cortez, a leading voice of her party’s progressive wing, and Ayanna Pressley, who likewise bashed corporate America during her campaign.

But those queries on Wells Fargo’s financing of private prisons and oil pipelines, businesses the bank has previously said it would pull back from, failed to land a major blow.

Democrats and Republicans took a broadly tough line, quizzing Sloan on the bank’s remediation efforts, personnel changes, risk management, culture and whether it should be broken up.

Opening the packed hearing, Waters recounted Wells Fargo’s missteps, saying the bank had failed to prove it had abandoned harmful policies.

“Wells Fargo’s ongoing lawlessness and the failure to right the ship, suggests the bank … is simply too big to manage,” she added, saying later in the hearing that Sloan should step down.

The committee’s ranking Republican Patrick McHenry made it clear that his party would not go soft on the country’s fourth-largest bank.

“You will hear bipartisan criticism of the actions you have taken and the failures that you have overseen under your watch,” he said.

Still, some Republicans later in the hearing acknowledged the bank’s efforts to change, with Representative Sean Duffy saying his colleagues had been too harsh on Sloan.

BETTER BANK?

The stakes had been high heading into the hearing for Sloan, a 31-year Wells Fargo veteran who was appointed CEO when John Stumpf retired soon after the sales practices scandal erupted in 2016.

The CEO has faced calls to step down from investors and politicians, including U.S. Senator Elizabeth Warren, a 2020 Democratic presidential contender.

Sloan’s prepared remarks emphasized changes the bank has made to culture, sales practices and risk management, as well as efforts to repay wronged customers.

“Wells Fargo is a better bank than it was three years ago, and we are working every day to become even better,” Sloan, 58, read from his written testimony.

At times Sloan expressed remorse over the bank’s scandals, noting he felt “terrible” that some servicemen and women had been harmed.

Sloan remained calm under pressure and rebuffed Waters’ claims that Wells Fargo should be broken up. He also said the bank had paid back all customers hit by improper mortgage rate-lock fees and gave a similar answer about auto insurance remediation.

But the CEO struggled to make the case that Wells Fargo is now a good corporate citizen amid repeated interruptions and aggressive, sometimes hectoring questioning from representatives including Democrats Brad Sherman and Stephen Lynch.

Sloan also appeared to frustrate some lawmakers by declining to disclose confidential information on the progress of some remediation efforts, and by failing to say categorically that Wells Fargo would never suffer another scandal.

If lawmakers are unhappy with what they heard, they could pressure the Federal Reserve to maintain restrictions imposed on the bank’s growth until governance and risk management improve.

Waters in her testimony said the Fed’s punishment had not changed the bank, adding: “regulators seem unwilling to take forceful actions.”

After the hearing, the Office of the Comptroller of the Currency, which last year fined Wells Fargo $1 billion for faulty mortgage and insurance products, echoed comments made by its head in October that the bank still had much work to do to. [L2N1WI189]

“We continue to be disappointed with Wells Fargo Bank N.A.’s performance … and its inability to execute effective corporate governance and a successful risk management program,” said OCC spokesman Bryan Hubbard.

The 2016 revelation that Wells Fargo created millions of fake customer accounts prompted regulatory probes into mortgage foreclosures, auto insurance sales and its wealth management businesses, resulting in billions of dollars in fines.

Reporting by Pete Schroeder and Imani Moise; Editing by Michelle Price and Meredith Mazzilli

[ad_2]

Source link